It is not straightforward to measure the performance of an investment strategy like ours.

That’s because:

- Our ethical criteria eliminates more than half of the companies that comprise popular indexes like the S&P 500 from consideration,

- “Sustainable” indices tend to concentrate their holdings in technology companies like Facebook, Tesla, and Google we also exclude on moral grounds, and

- We invest globally, which makes it difficult to compare our results with stock markets in any particular country.

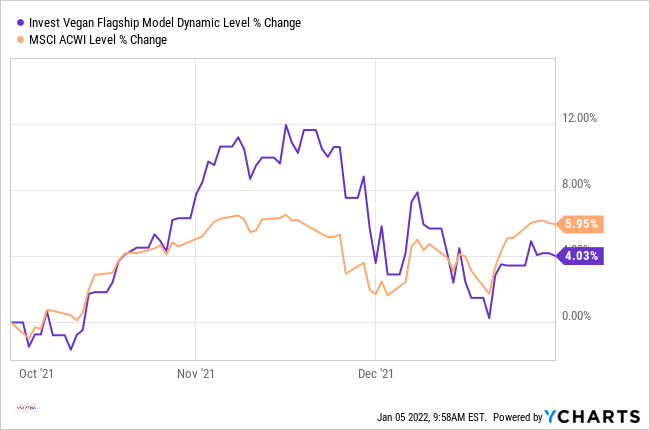

I could do a lot of complicated calculations to produce a more appropriate benchmark, but I don’t feel that would help you understand what’s happening in the portfolio any better. Instead, we will simply use the MSCI ACWI (a widely used global index) as our benchmark until a more straightforward approach emerges.

In the chart that follows, our portfolio’s daily returns (purple) for the quarter that just ended are presented alongside the index (orange). These returns are net of fees, and though I feel it’s important to share them with you regularly and transparently, I have to stress that they tell you close to nothing.

That’s because we are investing to build security and stability over the long term, not to produce a line that looks good on this chart over an arbitrary three month period. The pride and confidence that I have in our portfolio stems from the disciplined process that I followed to construct it and the deep research that has gone into each of its constituents.

Still, it’s nice that we were up 4.03% in our first quarter. Most people agree that it’s better to be up than down. But it bears mentioning that we will lose money sometimes, because we invest in securities that fluctuate in value over the short term for reasons that are beyond mortal understanding.

But that doesn’t mean there’s no point in doing the research. The portfolio described below represents my best thinking on how to position ourselves for success and stability over the coming years.

Thematic Overview and Positioning

This section describes each of our current positions as well as their thematic role in the portfolio.

Here are a few quick notes on how it’s composed so that you can use it effectively:

- Holdings that have been added in this quarter are denoted with an asterisk(*).

- Companies are listed under each theme in roughly descending order of their weighting in the overall portfolio.

- This is not meant to change very often. We make concentrated investments in high-quality companies that we intend to hold for long periods of time.

Without further ado, here are the companies that comprise our portfolio.

The Last Mile

Everyone has a right to reliable power, data, and a safe place to live. But it will take building, installing, and maintaining an awful lot of things to deliver on that. These companies get it done predictably and sustainably, adding meaningful stability to our portfolio in the meantime.

Our current holdings in this theme include:

- NextEra Energy, a regulated utility company and the world’s largest producer of wind and solar energy (NEE).

- UMH Properties, a real estate investment trust that specializes in high quality manufactured home communities with substantial affordability and environmental advantages over competing housing stock (UMH).

- Armada Hoffler, an integrated construction and property management company specializing in mixed-use developments (AHH).

- American Tower, a real estate investment trust specializing in the installation and maintenance of more than 180,000 cellular towers around the world (AMT).

- Two skilled contractor businesses that are well situated to support the ongoing electrification of our domestic grid: IES (IESC) and Quanta Services (PWR).

- *Ørsted A/S, the world’s largest developer of offshore wind power which is majority-owned by the government of Denmark (DNNGY).

- TopBuild, which specializes in insulating homes from extreme temperatures and boosting energy efficiency (BLD).

Overall, these holdings comprised roughly 30% of our portfolio as of January 2022.

From an investment risk standpoint, they are characterized by long investment cycles, significant backlogs of work to be done, and relatively stable, predictable returns on invested capital.

The Circular Economy

Our society needs to reimagine its approach to key resources. This includes reusing metals and minerals to avoid future extraction, avoiding excessive manufacturing, and managing whatever waste is created in the most eco-friendly way possible.

Our holdings in this theme include:

- Copart, the world’s leading online marketplace for damaged cars which allows efficient re-use of resources at national scale (CPRT).

- Cintas, a leading provider of uniform and facility supply rentals for businesses of various sizes (CTAS).

- *Tomra, the Norwegian inventor of reverse vending machines and maker of innovative recycling sorting machines (TMRAY).

- Waste Management, one of North America’s leading recyclers and the largest provider of integrated waste services in the United States (WM).

These holdings comprised roughly 14.3% of our portfolio as of January 2022.

As providers of essential services to businesses, they benefit from increased operational stability, limited competition, and a significant ability to pass on costs that may manifest due to inflation.

Economic Plumbing

Money makes things happen, and principled financial institutions play a significant role in ensuring that the right projects get funded and seen through to completion.

Our holdings related to this theme include:

- Agricultural Mortgage Corporation, better known as Farmer Mac. This lender was created by Congress to support the development of rural America by supporting regional electric and agricultural cooperatives. It is our single largest position at 9.7% of the portfolio (AGM).

- Silicon Valley Bank, a leading commercial bank for high-tech companies and startups used by roughly half of the United States’ venture-backed tech and life sciences companies (SVB).

- Signature Bank, an entrepreneurial New York based lender seeing significant deposit growth thanks to the success of Signet, its digital payment platform based on the Ethereum blockchain (SBNY).

- HDFC Bank, India’s largest private sector bank by assets. Known for astute credit underwriting and a range of innovative products, HDFC provides us an opportunity to support and benefit from the stunning growth of India’s domestic economy (HDB).

Taken together, these holdings comprise 18.6% of our portfolio as of January 2022.

As lenders, these firms are exposed to trends in the overall economy. I expect them to experience some credit losses during recessions, but each of them has experienced management teams, a proven business model, and a differentiated growth strategy that should allow them to support inclusive economic growth in a variety of macroeconomic environments.

Humanity Rises

Personal consumption spending is shifting towards companies that embrace our human needs and desires while adding comfort to our existence, which is meaningfully distinct from trend-driven models that tended to predominate before the pandemic.

Our holdings in this theme include:

- Crocs, perhaps the strongest brand that encourages people to “come as you are,” this company makes footwear that’s embraced by everyone from hypebeasts to dads who love to garden (CROX).

- E.L.F. Beauty, a leading cruelty-free beauty brand making products for “every eye, lip, and face,” the company enjoys excellent partnerships with a variety of retailers and growing international distribution for its affordable beauty products (ELF).

- *Nintendo, the legendary gaming innovator and creator of some of the least violent (and most fun) video game franchises on earth (NTDOY).

- Beauty Health Company, creators of the HydraFacial, an approachable skin treatment with material health and beauty outcomes, accelerating revenues, and a generational growth opportunity (SKIN).

- PLBY Group, famous for its bowtied bunny rabbit, today operates one of the world’s leading sexual wellness businesses and has made waves by embracing queer desire, entering the NFT marketplace, and launching a competitor to Onlyfans (PLBY).

- Cooper Companies, producers of contact lenses, hormone-free IUDs, and fertility products are building a diversified portfolio of personal care products that “improves lives, one person at a time” (COO).

Taken together, these businesses are 23.1% of our overall portfolio as of January 2022.

These firms are exposed to vagaries in consumer demand, which can be difficult to forecast as it remains unclear to what extent “business as usual” will resume. But given that each of them is associated with strong brands and products that help people to feel comfortable in their bodies, it’s reasonable to expect them to gain strength in the transition to the future, whatever form it takes.

Entrepreneurial Imagination

It’s always a good time to be an innovator, but now might be a better time than ever. These companies are commercializing advances in computing, material science, and biology to bring big things to market soon.

- Enphase, a market leader in microinverters that increase the efficiency of solar arrays in shady conditions and even enable continuous power production during outages without the need for batteries (ENPH).

- Alexandria Real Estate, a real estate investment trust that builds and manages research campuses close to urban environments and makes early-stage investments in innovative biotechnology companies (ARE).

- Ginkgo Bioworks, a specialist in genetically engineering organisms like yeast and bacteria for applications ranging from perfumes to vegan proteins and more sustainable agriculture (DNA).

These positions comprise 13.9% of our overall portfolio as of January 2022.

As technology-driven innovators, these companies encounter business risks associated with operating at the bleeding edge of human understanding. But they are far from unproven. All have enough cash on hand to weather a significant drawdown in the broader economy without being forced to raise capital at anything but advantageous terms.